Find Complete Details related to Professional Tax like – What is Professional Tax?, Article 276 in Constitution of India 1949, Deduction U/s 16 of Income Tax Act, Professional tax Rates, Professional Tax Forms, Professional Tax In India And Professional Tax Slab Rate etc. We also try to provide Professional Tax Slab Rates for AY 2016-17 for All States. Now you can scroll down below and check everything you want to know about Professional Tax.

What is Professional Tax?

Professional tax is levied by state government on the income earned by the way of profession, trade, calling or employmentThe power to levy professional tax has been given to the states by way of clause (2) of Article 276 of the constitution of India.

Professional tax is levied by particular Municipal Corporations and majority of the Indian states impose this duty. It is a source of revenue for the government. The maximum amount payable per year is INR 2,500 and in line with tax payer’s salary, there are predetermined slabs. It is also payable by members of staff employed in private companies. It is deduced by the employer every month and sent to the Municipal Corporation. It is a mandatory to pay professional tax. The tax payer is eligible for income tax deduction for this payment

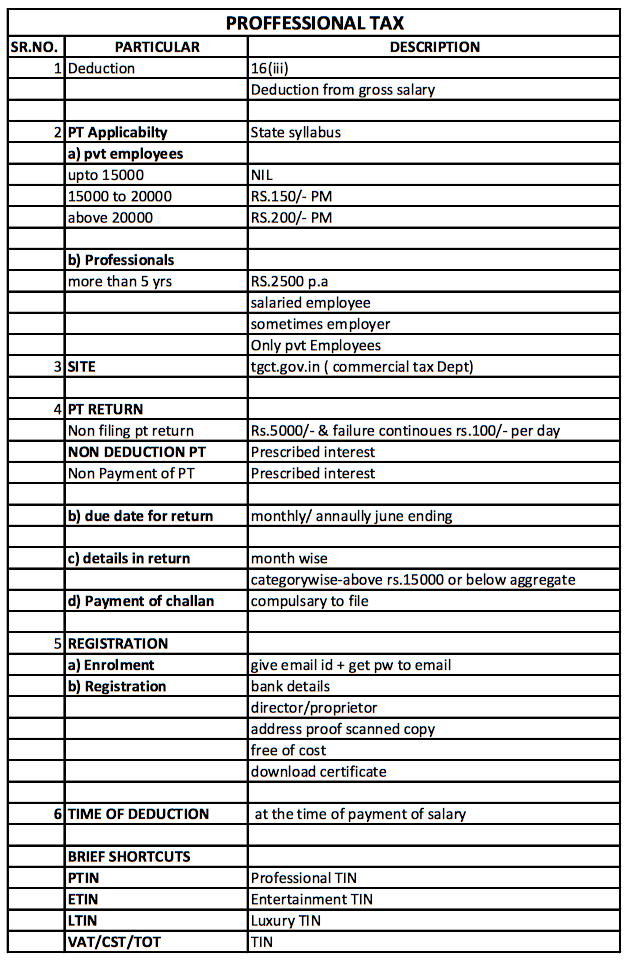

Professional Tax Brief Telangana & Andhra Pradesh

Professional Tax Due Dates All States

Applicability of Professional Tax

Applicability of Professional Tax as per the Constitution of India: Article 276 of the Constitution of India provides that “there shall be levied and collected a tax on professions, trades, callings and employments, in accordance with the provisions of this Act. Every person engaged in any profession, trade, calling or employment and falling under one or the other of the classes mentioned in the second column of the Schedule shall be liable to pay to the State Government tax at the rate mentioned against the class of such persons in the third column of the said Schedule. Provided that entry 23 in the Schedule shall apply only to such classes of persons as may be specified by the State Government by notification from time to time.

Article 276 in Constitution of India,1949

Notwithstanding anything in Article 246, no law of the Legislature of a State relating to taxes for the benefit of the State or of a municipality, district board, local board or other local authority therein in respect of professions, trades, callings or employments shall be invalid on the ground that it relates to a tax on incomeThe total amount payable in respect of any one person to the State or to any one municipality, district board, local board or other local authority in the State byway of taxes on professions, trades, callings and employments shall not exceed two hundred and fifty rupees per annum: Provided that if in the financial year immediately preceding the commencement of this Constitution there was in force in the case of any State or any such municipality, board or authority a tax on professions, trades, callings or employments the rate, or the maximum rate, of which exceed two hundred and fifty rupees per annum, such tax may continue to be levied until provisions to the contrary is made by Parliament by law, and any law so made by Parliament may be made either generally or in relation to any specified States, municipalities, boards or authoritiesThe power of the Legislature of a State to make laws as aforesaid with respect to taxes on professions, trades, callings and employments shall not be construed as limiting in any way the power of Parliament to make laws with respect to taxes on income accruing from or arising out of professions, trades, callings and employments

Deduction U/s 16 of Income Tax Act

Any amount paid to state government as professional tax is allowed as deduction under section 16(iii) of Income tax Act.Section 16(iii):- Deduction is available only in the year in which professional tax is paid. If professional tax is paid by employer on behalf of employee, then first it is included in the salary of the employee as a “Perquisite” and then the same is allowed as deduction on account of “Professional Tax” from gross salary. There is no monetary ceiling under Income tax Act(under the Article 276, State government cannot impose more than Rs 2500 Per annum as professional tax).Whatever professional tax is paid during the year is deductible.

Deducted and Paid By?

In case of salaried and wage earners, the professional tax is liable to be deducted by the employer from the salary/wages and the same is to be deposited to the state government.In case of other class of individuals, this tax is liable to be paid by the employee himself.

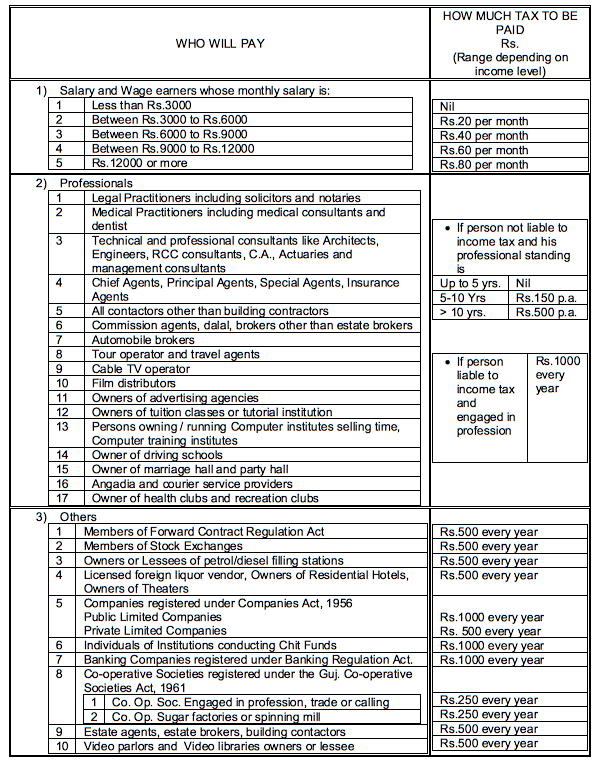

Professional tax Rates

If you are salaried employee earning above Rs.12000 per month then you are liable to pay Rs.200 per month. The Annual Professional Tax is Max Rs.2500.Please Note these Professional Tax Rates is Only as per Gujarat State (We Provide Professional Tax Slab Rates for All States in Next Article)

(a) rupees two hundred per month except for the month of February (b) rupees three hundred for the month of February

Professional Tax in Karnataka:

Professional Tax in West Bengal:

Professional Tax in Madhya Pradesh:

Professional Tax in Tamil Nadu:

Professional Tax in Andhra Pradesh:

Professional Tax in Gujarat:

Professional Tax in Odisha:

Registration of Professional Tax

The Employer has to get registered even if he is responsible to deduct tax from the salary of one employee.Form No 1 is the Application form for Registration.The time limit for registration is 60 days from the date of accruing liability under the Act.The Employer has to get separate registration for each of his Branch

Deposit of Amount Deducted

Employers covered under the jurisdiction of “State Government” as Designated authority shall pay in the treasury by Challan through the bank. Other employers shall pay at the place of payment declared by the Designated Authorities concerned.If an employer has employed more than 20 employees, he is required to make payment within 15 days from the end of the month. However, if an employer has less than 20 employees, he is required to pay quarterly(i.e. by the 15th of next month from the end of the quarter).

Interest Provisions

Fails to get Registration – He will be liable to a penalty of Rs.20/- per day under Section 5(5) for the period during which he remains unregistered. Interest on Late Payment of Professional Tax – He is liable to pay interest at the rate of 18 % per annum for such delayed period along with penalties prescribedNon Deposition of Amount. – The officials have power to recover such amount along with applicable penalty and interest from the assets of such defaulter. Moreover they can attach his bank account also. In serious cases, prosecution case (police case) also can be filed.

Due Date for Payment of Professional Tax

If less than 20 or less 20 Employees , than Due date for payment of Professional Tax is 15th day from the end of quarter If More than 20 Employees , than Due date for payment of Professional Tax is 15th day from the end of Month Return Filing As Per Gujarat State

A monthly return in Form No.5 is to be filed by 15th of next month, if the number of employees is more than twenty. Where number of employee is less than 20, only an annual return in Form No.5AA is required to be filed.If Any Registration holder wants to file Annual return then he can file if he has obtain special permission from the authority by applying in the FORM 5B for this purpose.

Gujarat Professional Tax Schedule

click here do download full file in pdf

Professional Tax Forms (Gujarat Commercial Tax)