A non-resident taxable person shall electronically submit an application, along with a valid passport, for registration, duly signed, in form GST REG-09, at least five days prior to the commencement of business at the Common Portal either directly or through a Facilitation Centre – Rule 6(1) of Registration Rules.

GST Registration by Non Resident Taxable Person

In GST regime, registration is fully online and any legal person wishing to register will have to access the GST system for the same. A new applicant would be allowed to apply for registration without prior enrollment. Scanned copy of prescribed documents is required to be filed along with the application for registration. Once a complete application is submitted online acknowledgement Number would be generated and intimated to the applicant. The application form will be passed on by GST portal to the IT system of the Central and Model 1 State tax authorities for onward submission to appropriate jurisdictional officer (as selected in the form) along with specified information. On receipt of application, the tax authority would forward the application to jurisdictional officers who shall examine whether the uploaded documents are in order and respond back to the common portal within 3 working days, using the Digital Signature Certificates Once the application is approved and GSTIN is generated, the same along with GSTIN and temporary Password will be sent to the authorized signatory. Thus, the registration of new taxpayers will be done on the GST system; however, the approval of the registration and Registration Certificate will have to be provided by the State or Central Tax Authorities to which the application is forwarded for processing. In case registration is rejected, the applicant will be informed about the reasons for such rejection through a speaking order..

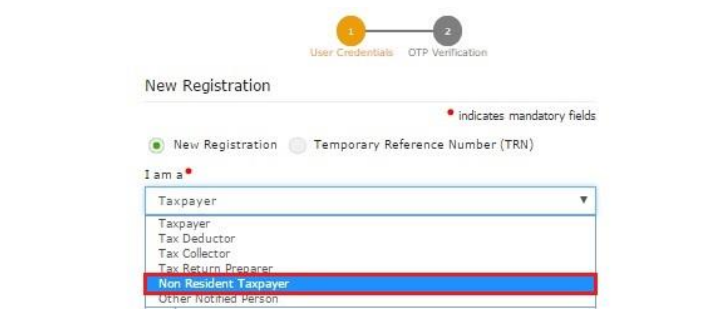

I am a Non-Resident Taxable Person. How do I obtain a GST Registration?

A non-resident taxable person would be allowed to apply for registration. For the same, he first need to fill Part-A of the Form, which consists of Legal Name of Non-resident Taxable Person, PAN (if any), Email Address and Mobile Number of the Authorized Signatory. Once, these are validated, Temporary Reference Number (TRN) will be generated and sent to the Applicant. Based on the same, he would be able to retrieve the application and fill balance information in Part B of the form. On successful submission of Form with authentication, Application Reference Number (ARN) would be generated and intimated to the applicant. Once the application is approved and GSTIN is generated, the same along with GSTIN and temporary Password will be sent to the Authorized Signatory. Remember to select Non-Resident Taxpayer in the mandatory dropdown – ‘I am a Once, these are validated, a Temporary Reference Number (TRN) will be generated and sent to you. Based on the generated TRN, you will be able to retrieve the application and fill balance information in Part B of the form. On successful submission of Form with authentication, Application Reference Number (ARN) will be generated and intimated to you. Once the application is approved and the GSTIN is generated, the same along with the temporary Password will be sent to the Authorized Signatory listed in your application. These credentials can be used to access the GST Common Portal subsequently. No, PAN is not mandatory for obtaining temporary registration as a Non-Resident Taxable Person however, you must have an authorised signatory who is an Indian citizen with a valid PAN card. Do I need an Indian mobile number to obtain a temporary registration as a NonResident Taxable Person? No, you do not need an Indian mobile number to obtain a temporary registration as a NonResident Taxable Person however, you must have an authorised signatory who is an Indian citizen with a valid Indian mobile number. Do I need a place of business in the state I intend to carry out business in? Yes, it is mandatory for you to secure a place of business in the state you intend to obtain the registration before you apply for the registration. By when should I apply for a Registration as a Non-Resident Taxable Person? You should apply for Registration as a Non-Resident Taxable Person 5 days prior to the date of commencement of business How long is the Registration as a Non-Resident Taxable Person valid? Registration as a Non-Resident Taxable Person can be granted for a maximum of 90 days.

Can I extend my Registration as a Non-Resident Taxable Person?

Yes, you can extend your Registration as a Non-Resident Taxable Person once for an additional period of 90 days if you apply before the expiration of the initial period. I have already extended my initial registration once and cannot extend it a second time as per prevailing laws. What do I do if my extension is about to expire and my business has not concluded? In such a case, you are required to obtain registration as a normal taxpayer in the concerned state. The moment I select Registration as a Non-Resident Taxable Person option the New Registration Application forms asks me to fill a GST Challan. Why? In case of Registration as a Non-Resident Taxable Person, you are required by law to deposit the tax in advance based on the estimated turnover for the period for which the registration has been obtained. A GSTIN will also be generated and prefilled in the challan. The status of this GSTIN will be provisional until your application is approved by the tax authority and the registration is officially granted. Is there a fixed amount I must deposit with the GST authorities before taking a Registration as a Non-Resident Taxable Person? No, you are required by law to deposit the tax in advance based on the estimated turnover for the period for which the registration has been obtained.